a Nordic-branded wellness product range on a Thai retail shelf

Nordic health brands enter Thailand with a product, not a plan.

The Thailand wellness market generated THB 1.2 trillion in 2024, roughly USD 35 billion, and is growing at 8.5% per year through 2028. Urban consumers in Bangkok, Chiang Mai, and Phuket are buying supplements, wellness devices, and functional foods in increasing volumes. A Nordic company with clean formulations and credible home market positioning finds it hard not to look at this and see opportunity.

What they underestimate is how different the path into that market is from any previous entry experience.

Mistake one: the regulatory timeline assumption

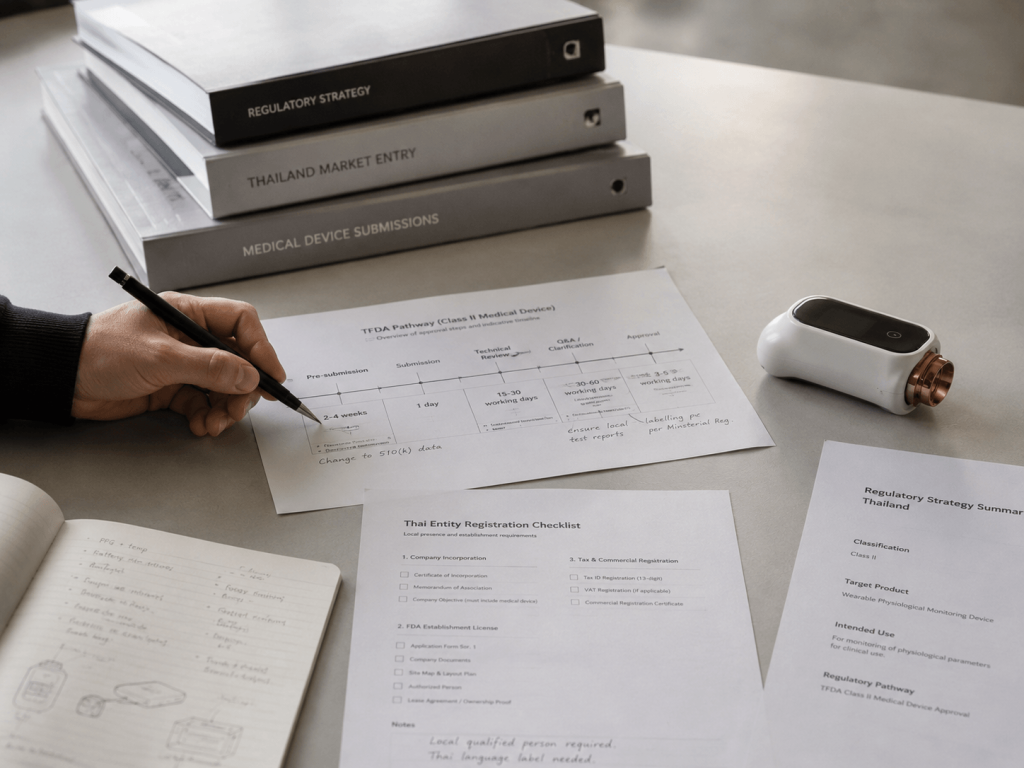

The Thai Food and Drug Administration requires product registration before any product can be sold. For health supplements and Class II medical devices, that process averages 6 to 12 months through the ORYOR digital portal, and up to 18 months for more complex products. Cosmetics on the ASEAN harmonised track can move through in 3 to 6 months, but still represent a substantial lead time relative to most European markets.

This is not a bureaucratic inconvenience. It is a structural constraint that reshapes the entire year one calendar.

The most common mistake is arriving in Thailand with product in transit or inventory already ordered, assuming registration can run concurrently with market preparation. It cannot. TFDA will not accept a product registration from a foreign company without a locally established Thai entity, and entity registration through the Department of Business Development takes an additional 3 to 6 months. The two processes must run sequentially. The earliest a Nordic health brand can realistically expect to sell legally in Thailand is 9 to 18 months after the decision to enter.

Companies that do not account for this front-load their costs before revenue exists. The ones that plan for it use the registration period productively: building distributor and retail relationships, completing consumer research, and finalising Thai-market packaging, all before the first legal sale.

Mistake two: the distributor lock-in

Thailand’s pharmaceutical and health distribution landscape is concentrated. Five major players control approximately 60% of health product imports. For a Nordic brand entering without established contacts, signing with one of these distributors is the obvious first move.

The problem is not the distributor. It is the exclusive agreement.

Nordic brands routinely sign exclusive territory agreements that make the distributor the sole route to market. The distributor, carrying a large portfolio of established brands, allocates commercial energy to products that already have velocity. A new Nordic entrant with no local track record competes for attention inside the distributor’s own portfolio. Without minimum performance clauses, reporting obligations, and a defined review timeline, a brand can sit largely inactive for 12 months with no mechanism to intervene.

The channel strategy problem runs deeper. Thai consumers under 45 buy wellness products primarily through modern trade, Tesco Lotus, Central, Boots, and e-commerce platforms like Lazada and Shopee. A distributor relationship does not automatically unlock these channels. Each requires a separate commercial negotiation, and most require the brand to initiate those conversations directly. A company that delegates all market activity to a distributor is invisible in the channels where its target consumer actually shops.

The better approach is a phased structure: a non-exclusive or limited-exclusivity agreement with a clear performance review at month nine, running alongside direct e-commerce activation and at least one modern trade listing negotiated in parallel from day one.

Mistake three: the credibility translation failure

Nordic health brands carry genuine credibility at home. Clean ingredients, verifiable certifications, sustainability credentials. In Thailand, that credibility is invisible until it is rebuilt in a language the Thai consumer can read, literally and culturally.

TFDA Notification No. 388/2023 requires bilingual labelling. All ingredient lists, usage instructions, and required disclosures must appear in both Thai and English. EU-compliant labelling is not TFDA-compliant labelling. The translation is not a design afterthought, it is a regulatory requirement that must be completed before product registration.

Claim restrictions add another layer. Standard European wellness marketing language, “supports cognitive function”, “promotes digestive health”, constitutes a disease treatment claim under TFDA rules if made without clinical substantiation. Many Nordic brands write their Thai packaging using their European copy as a starting point, then discover that several of their core claims require either clinical evidence or removal. Reprinting and resubmitting extends the registration timeline further.

Beyond compliance, the credibility chain in Thai wellness retail works differently from Europe. Nordic brands are not household names in Thailand. Consumers in pharmacy chains and wellness stores respond to third-party validation: pharmacy chain endorsements, physician or pharmacist recommendations, and influencer credibility within the health category. A brand without any of these local signals, however strong its European reputation, does not have the credibility infrastructure that drives purchase in the Thai market.

Building that infrastructure requires time and local partnerships: a medical professional willing to be cited, a health content creator with a genuine wellness audience, and a pharmacy buyer who has chosen to give shelf space based on a relationship rather than a track record.

What year one should actually look like

The Nordic health brands that succeed in Thailand do not arrive faster than the market allows. They use the regulatory lead time to build what the Thai market requires.

Entity registration before product finalisation. TFDA timeline mapped before inventory is committed. A channel plan, distributor terms, modern trade targets, e-commerce setup, before any distribution agreement is signed. A localisation plan covering label language, claim structure, credibility partnerships, and consumer communication, all executed before the product reaches a Thai shelf.

Year one in Thailand is a construction year, not a sales year. The brands that treat it as a sales year tend not to make it to year two.